Section 179 At a Glance – New for 2012

Section 179 At a Glance – New for 2012

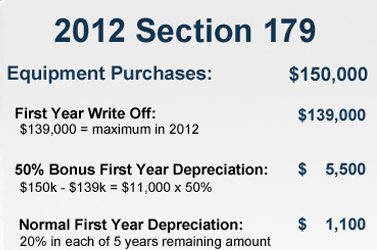

2012 Deduction Limit of $139,000 is good on new and used equipment, as well as off-the-shelf software.

2012 Limit on equipment purchases of $560,000 is the maximum amount that can be spent on equipment before the Section 179 Deduction available to your company begins to be reduced.

More Detailed Section 179 Information

What is the Section 179 Deduction?

Most people think the Section 179 deduction is some mysterious or complicated tax code. Essentially, Section 179 of the IRS tax code allows businesses to deduct the full purchase price of qualifying equipment and/or software purchased or financed during the tax year. That means that if you buy (or lease) a piece of qualifying equipment, you can deduct the FULL PURCHASE PRICE from your gross income. It’s an incentive created by the U.S. government to encourage businesses to buy equipment and invest in themselves. Section 179 is one of the few incentives included in any of the recent Stimulus Bills that actually helps small businesses, and millions of small businesses are taking section 179 and getting real benefits.

Limits of Section 179

Section 179 does come with limits – there are caps to the total amount written off ($139,000 in 2012), and limits to the total amount of the equipment purchased ($560,000 in 2012). The deduction begins to phase out dollar-for-dollar after $560,000 is spent by a given business, so this makes it a true small and medium-sized business deduction.

Who Qualifies for Section 179?

All businesses that purchase, finance, and/or lease less than $560,000 in new or used business equipment during tax year 2012 should qualify for the Section 179 Deduction. To qualify for the Section 179 Deduction, the equipment and/or software purchased or financed must be placed into service between January 1, 2012 and December 31, 2012.

What Software Qualifies?

For basic eligibility, the software must meet all of the following general specifications:

– The software must be financed.

– The software must be used in your business for income-producing activity.

– The software must have a determinable useful life.

– The software must be expected to last more than one year.

In addition, these three specific stipulations must be met:

– The software must be readily available for purchase by the general public.

– The software must be subject to a non-exclusive license.

– The software must not have been substantially modified.

Material goods that generally qualify for the Section 179 Deduction

For the Section 179 Deduction, the equipment listed below must be purchased and put into use between January 1, 2012 and December 31, 2012.

– Equipment (machines, etc) purchased for business use

– Tangible personal property used in business

– Business Vehicles with a gross vehicle weight in excess of 6,000 lbs (Section 179 Vehicle Deductions)

– Computers

– Computer “Off-the-Shelf” Software

– Office Furniture

– Office Equipment

– Property attached to your building that is not a structural component of the building (i.e.: a printing press, large manufacturing tools and equipment)

– Partial Business Use (equipment that is purchased for business use and personal use: generally, your deduction will be based on the percentage of time you use the equipment for business purposes).

Imformation cited from http://www.section179.org/section_179_deduction.html